ALL POSTS PRIOR TO 2021 HAVE NOT BEEN REVIEWED NOR APPROVED BY ANY FIRM OR INSTITUTION, AND REFLECT ONLY THE PERSONAL VIEWS OF THE AUTHOR.

December 29, 2020

A SCHOLAR FINANCIAL SPECIAL REPORT

PART TWO:

THE ECONOMY AND THE CAPITAL MARKETS;

AN INVESTMENT PORTFOLIO FOR THE FUTURE

From Ron A. Rhoades, JD, CFP

E-mail: ron@scholarfinancial.com (clients and prospective clients only)

E-mail: ron.rhoades@wku.edu (students, family, colleagues, friends)

Tuesday, December 29, 2020

Dear Clients, Students, Family and Friends:

In Part One of my Special Report, delivered a few weeks ago, I conveyed information about COVID-19, and sought to answer some questions regarding vaccinations. Obviously, the impact of COVID-19 on our U.S. economy and global economy has been severe, and further economic downturns are likely during the long Winter and Spring of 2020-2021. Yet, as discussed, we can hope that the pandemic will largely be behind us by the summer of 2021, and that economic activity will increase over time.

In today’s Part Two of my Special Report, I address the impact of the pandemic on the U.S. economy and global economy, and look forward beyond the near-term impacts to discuss longer-term expected developments. I also touch on the uncertainty caused by mutations to the COVID-19 virus.

I then explore the future returns of various asset classes, showing that the U.S. stock market is overvalued by a tremendous amount, but that most of this overvaluation occurs in “growth stocks.” (The equity portion of my clients’ portfolios is tilted toward “value” stocks.)

I also discuss changes occurring with several mutual funds and exchange-traded funds (ETFs) from Dimensional Funds Advisors, that will bring lower fees as well as greater tax-efficiencies to some of my clients.

TABLE OF CONTENTS

A. THE U.S. AND GLOBAL ECONOMY IN THE NEAR TERM

1. Will the “rebound” be “V-shaped” or “U-shaped” or something else?

2. Service Businesses, Especially Small Ones, Have Been Hit the Hardest

3. Unemployment, and Unemployment Benefits.

4. Economic Activity to Rebound in 2021?

5. Perspective on the Threats from COVID-19 Mutations.

B. DEVELOPMENTS AFFECTING THE ECONOMY IN THE LONG TERM

1) Increased Corporate Cash Holdings.

2) Shift of Working from Large Cities to Rural Areas.

3) Decrease in Birth Rates – U.S. and Globally.

4) A Greater Understanding that In-Person Education is Optimal, for Many Students.

5) Increase in Productivity, Via Application of Technologies.

6) Wealth Inequality, Wealth Used to Influence Public Policy – and Their Dangers.

7) Positive Long-Term Trends.

C. THE FUTURE PROJECTED LONG-TERM RETURNS OF STOCK ASSET CLASSES

1) In Summary, The Expected Long-Term Returns of Some Stock Asset Classes Appear Favorable, but the Prospects of Positive Returns in Other Stock Asset Classes Appear to be Quite Dismal.

2) On the Analytical Foundations of These Projected Returns, and the Inherent Uncertainties Present in Projecting 10-Year and 15-Year Asset Class Returns

3) Investment Asset Class Return Projections (by Ron, and by Others)

4) U.S. Large Cap Stock Valuations: The Shiller CAPE10 Ratio Indicates an Extreme Over-Valuation

5) But, Small Cap Value Stocks Appear Reasonably Valued.

6). Emerging Markets Value Stocks.

D. BONDS, C.D.’S, AND INTEREST RATES.

E. DIMENSIONAL FUNDS ADVISORS: DECREASED FEES; ETFS.

A “V-shaped recovery implies a quick rebound, while a “U-shaped recovery” implies a long time to recovery.

As I stated many months ago, and as I continue to believe, we shall see more of a long “W-shaped” recovery, with a long right upwardly sloping tail for the last part of the “W.” We already hit the first bottom, and the middle peak, and we are now on the second downturn. As you know, we are seeing a resurgence in COVID-19 cases, and this will result in another (but less deep) economic downturn over the winter months. Sometime in the spring the economy will again commence its recovery, but it will take time to form new businesses to replace the many that have failed, and will fail, during 2020 and early 2021.

It may take many months for things to return to a state of “normalcy.” Part of the problem is that the COVID-19 “fire” is raging hot, currently. While the vaccines are like water coming out of a fire hose, it will take a great deal of that “water” to put out the flames. Hence, some experts have suggested that 85% or more of the U.S. population will need to establish some form of immunity to COVID-19 for the disease to be reduced to very low rates of transmission. And these experts suggest a time frame of five to eight months for this to occur – and that is if a very large percentage of Americans choose to be vaccinated.

The fact of the matter is that the U.S. economic recovery remains tied to our ability to defeat COVID-19 – through vaccinations, continued social distancing measures, and (especially) the wearing of masks.

As Forbes contributor Pamela N. Danziger recently wrote, in her article “Half Of Small Retailers May Be Forced Out Of Business With More Restrictions Threatening,” business providing personal services have been especially hard-hit.

According to an article appearing on Dec. 14, 2020, in The New York Times (Kerry Hannon, “It’s a Terrible Time for Small Businesses. Except When It’s Not.”), about 28.8 percent of small businesses were already closed for good as of mid-November.

According to the November 2020 data, 10.7 million Americans are classified as” unemployed.” But, when measuring unemployment by a broader measure, the unemployment rate jumps from 6.7% to 10.0%. And measures to stem the current explosion of COVID-19 cases will likely cause the unemployment rates to spike upward in the next few months, at least somewhat.

Fortunately, there are unemployment benefits, which have tempered the economic decline and enabled some unemployed to financially survive during 2020. Unemployment benefits were extended through the end of 2020 by the U.S. Congress, earlier this year, with another extension just signed into law for the next few months. However, for at least a few weeks, 12 million Americans currently receiving unemployment benefits could see their benefits lapse; this is because in many states it can take weeks to continue benefits under the recently passed legislation, due to outdated state systems.

The stimulus checks and extended unemployment benefits may not be enough to offset a significant increase in residential mortgage foreclosures in 2021. Seriously past-due (90+ days) mortgages remain 1.8 million above the pre-pandemic level of about 450,000.

In addition, of the 44 million U.S. households that rent their homes, only 75.4% of those households have made full or partial rent payments (some landlords allow partial rent payments) for December 2020. As eviction bans end in mid-2021, we may see a significant rise in the number of individuals and families evicted from their homes.

When 62 economists were surveyed to obtain the mean future projection for U.S. economic growth in 2021, the slowest projection of U.S. economic growth came from A.C. Cutts, who indicated only a 1.9% increase in GDP over the next four quarters (2020Q4-2021Q3).

While I am not as pessimistic as AC Cutts, I do believe that the “V” shape indicated by the survey mean will be a more like the shallow decline in the second part of a “W” as indicated by A.C. Cutts, but with a faster rebound starting in the second quarter of 2021 than his projection indicates.

However, if Congress were to increase the stimulus checks just passed, from $600 a person to $2,000 a person, this would likely also boost the recovery.

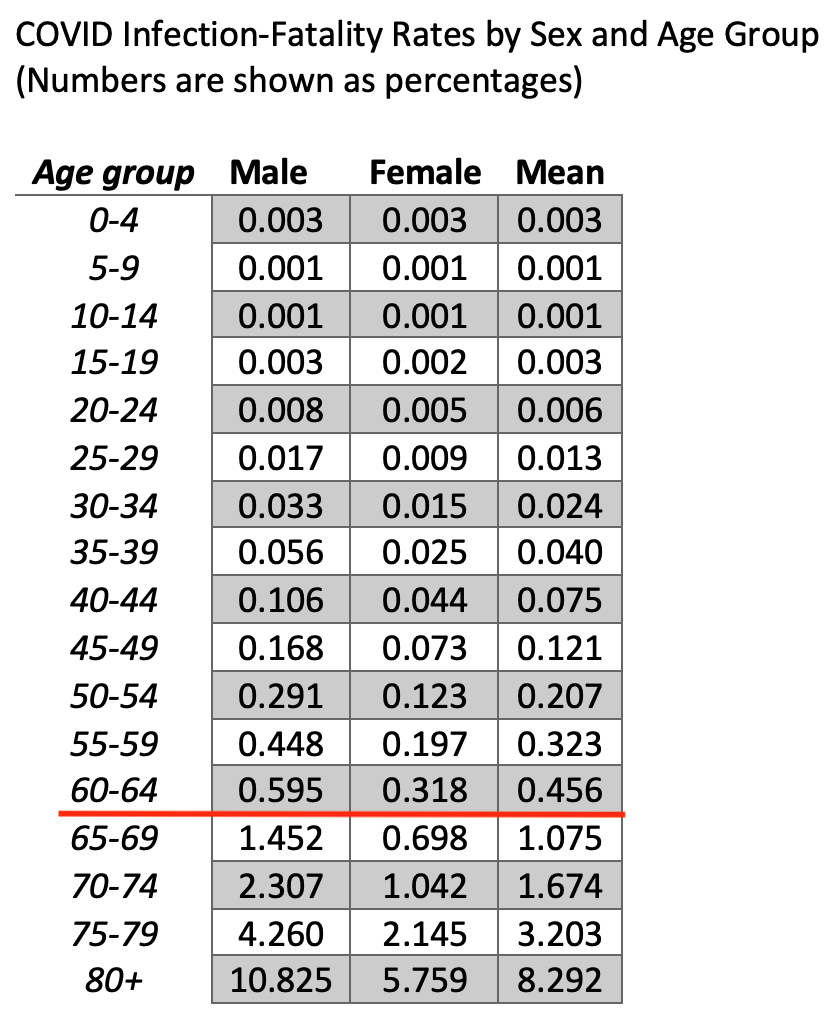

During this past month news has spread of mutations to COVID-19 which apparently increased the transmission rate of the disease. While no evidence yet exists that the disease mutations, found in the United Kingdom and in South Africa, cause a more severe inflection, the fact that many mutations have emerged in just the first year of the COVID-19 disease raises a number of troubling questions. For example, will the current vaccines be effective against new strains of COVID? And … how long will the current vaccinations offer protection against COVID – i.e., will a new vaccination be required every year, or even more often?

Thousands of different mutations in the COVID-19 virus have already occurred. However, for the virus to mutate sufficiently to not be affected by the Pfizer-BioNTech and Moderna vaccines, it would not only have to change significantly, but do so in one specific area of the virus, the spike protein that latches onto cells in the body. It is not inconceivable that the virus could change in this way; viruses mutate all the time.

Volunteers who received the Moderna had more different types of antibodies in their blood than did people who had been sick with COVID-19, but not more in terms of numbers of antibodies. Interestingly, the Pfizer-BioNTech and Moderna vaccines induce an immune response only to the spike protein carried by the coronavirus on its surface. But each person who is actually infected by COVID-19 (and who survives) produces within their body a large, unique and complex repertoire of antibodies to this protein. But it is not just the different types of different antibodies produced – it is also their strength and numbers. The Pfizer-BioNTech and Moderna generally produce a very large number of a single antibody, far in excess of the total number of antibodies produced by infected persons. Vaccines for some pathogens, like pneumococcal bacteria, induce better immunity than the natural infection does. Early evidence suggests that the Covid-19 vaccines may fall into this category.

Also, we know that there are very, very, few persons who suffer a severe reaction to the vaccines. In contrast, intentionally contracting COVID-19, to generate different types of antibodies, is like Russian roulette … you simply cannot predict if a person will have a minor reaction to the virus or a more severe reaction, requiring hospitalization, resulting in severe long-term health consequences, or leading to death. In conclusion … get vaccinated, when you can; don’t wait to catch the disease.

Several experts have expressed the view that mutations sufficient to counter the effectiveness of a vaccine would take years to occur, not months. Hence, it appears likely that the current Pfizer and Moderna vaccines, which are said to have 95% or greater effectiveness against the disease, will likely be in use for at least several years to come.

If and when a mutation occurs that renders current vaccines ineffective, pharmaceutical companies could have a new version of the vaccine ready within a few months. During this period, however, we might see social distancing and other measures implemented to slow the spread of any new disease variant. And that would impact the economy of the regions affected by any mutated virus – at least in the short-term.

It is this fear of future disruptions that is driving companies and firms to re-visit how people work together. Are desks spread apart sufficiently? Is air flow in the workplace sufficient? Should windows exist in office buildings to facilitate the entry of “fresh air”? How far apart should people stand or work in a production line? How might contingency planning better protect firms from production stoppages … such as by planning for more people to work from home during the next pandemic, or spreading workers on production lines out (and possibly using more shifts)? A great deal of effort is now going into planning at companies, as they try to assess and counter the risks of not just this pandemic, but possible future ones as well.

Those who contracted COVID-19 should still get the vaccine. The number of antibodies generated within a person’s body varies with the severity of the illness. In people who are only mildly ill, the immune protection that can prevent a second infection may wane within a few months. In contrast, the vaccines are known to generate a very large amounts of antibodies … often 200 times the number of antibodies generated when someone was infected. The immunity a person obtains from the vaccine is likely to last a lot longer than the immunity gained by a person who contracted COVID-19 and since recovered.

When is a person who has been vaccinated then protected? The Pfizer and Moderna vaccines require two doses, given two weeks apart. While some protection is provided by the first dose, once the second dose kicks in at about one week after the second shot, both the Pfizer and Moderna vaccines have shown in studies to be about 95% effective in preventing COVID-19.

However, being vaccinated does not mean you should not wear a mask and practice social distancing. Scientists don’t yet know if the virus can be transmitted by someone who has received the vaccine and generated sufficient antibodies. It is possible that the virus could reside in an infected person’s upper respiratory tract, and spread to others, at least for a period of time – even if that person has been vaccinated and generated antibodies sufficient to combat the disease (as to contracting the disease herself or himself).

How long will a vaccination continue to be effective? It’s possible that coronavirus vaccinations will become an annual event, just like the flu shot. Or it may be that the benefits of the vaccine last longer than a year. We simply don’t know at this point.

There are many potential implications for the long-term, some positive, and some negative, for the U.S. and global economies.

Following the Great Financial Crisis of 2008-9, larger corporations increased their cash holdings substantially. I anticipate that corporations, to better ensure their survival should another pandemic occur, will again be more conservative in terms of holding cash.

Hopefully corporations will also decrease their outstanding debt, although with the cost of debt being so low (as interest rates are low), this may not occur.

As you have likely observed, many workers in large cities – who now work from home – have moved out of high-rent areas in large cities to more rural areas. With substantially increased use of providing services via online connections has occurred, there will certainly be more individuals desiring to work from home, and more companies that will facilitate such.

However, I suspect that over the years ahead a shift back into workplaces will occur. About 70% of all work done in corporations today by those who work in offices is done in teams (a substantial increase from 40%, just a few decades ago). Also, training and mentoring new employees is best done in-person. In the future many corporations may desire to have employees who have the flexibility to either work from home or come into the office, in the years ahead. Although the costs of having employees in the office will increase (due to increase separation, leading to larger workspaces), companies will see the value in having employees in the office, at least for a significant portion of their time.

Birth rates in the United States have been steadily declining over many decades. Following the 2008-9 Great Financial Crisis, birth rates continued their decline.

I suspect birth rates will continue to decline, especially in 2021, due to the pandemic and the financial impacts felt by many young couples. With the cost of raising one child estimated to be $200,000 or greater from birth to age 18, here with in the United States, more and more couples may decide to not have children, or to have fewer children.

This long-term demographic trend is not isolated to the United States. Globally birth rates have declined, and are projected to decline further, as illustrated the chart at right.

By 2030 and later, despite the advances in technology that lead to less utilization of workers in many sectors of the economy, there will likely be increased shortages of trained technicians, as well as of college graduates in many fields.

Less restrictive immigration policies will likely alleviate some, but not all, of these future shortages of skilled workers.

From K-12 through college, a far greater number of students have now participated in online classes. One might think that this will lead to a substantial movement away from in-person instruction in the years ahead, but I suspect that the embrace of online education will be modest, at best. Why? Because online education for most students is not as effective in achieving learning outcomes.

For K-5 students, several studies report a dramatic decrease in learning outcomes for students this past year.

Through personal experience, I can attest to the fact that very few university students felt that their learning via online instruction came close to matching that seen in the classroom, despite a monumental effort by many university professors to learn and implement best practices in online education.

One might question why this exists. The reality is that teachers and professors do more than just provide instruction. They also serve as mentors and advisors and role models and motivators.

There is also a certain “magic” that results from teacher/professor – student interactions, and from peer-to-peer learning activities. These conditions are difficult to replicate online.

For many students lacking self-discipline, in-person instruction is better to hold them accountable for their work efforts, from day-to-day.

I have always believed that attending college is not just about the acquisition of knowledge. It is also about developing all-important skills, and maturing socially and in other ways. Still, the university experience can and should evolve further, and not just because of continued decades-long declines in state support for higher education. More project-based learning, small group instruction within hybrid courses, internships, and greater flexibility to customize curricula to better meet the needs of students and their potential future employers, along with better instructional methods designed to achieve long-term retention, can be undertaken. We can also encourage students to major in degree paths and/or achieve certificates that better meet the employment shortages likely to occur in many areas by 2030 and beyond.

Demographic trends don’t bode well for universities after 2025. Due to declines in the college-age population, a decrease in the number of students attending college by 10% or so (more in some areas of the country, less in other areas) will occur. As a result, smaller colleges will continue to close. And larger universities who don’t adequately plan for the expected need for “downsizing” will become financially stressed.

The coronavirus pandemic is accelerating the uptake of automation in the workplace, putting jobs at risk – especially in the sectors that have been hit hardest.

Greater deployment of technology in manufacturing will aid the movement toward U.S.-based manufacturing operations. Still, to make labor costs in the U.S. competitive, many companies need to be able to produce the same quantity of product with about half of the employees that would be needed in a similar factory in China. However, wages in China are increasing. Also, there is a greater realization that China’s communist government and its varying policies, along with trade disputes with the U.S. and other countries, can lead to risks of supply chain disruptions.

There is a lot of venture capital today that is devoted to trying to automate farm labor tasks, particularly relating to the harvesting of crops. Robotics are also increasingly used in manufacturing. Artificial intelligence (while still in its infancy) is already leading to the automation of other processes, such as responses to customer inquiries, that previously were quite labor-intensive.

A lot has been written about wealth inequality in recent years. There is no doubt that long-term trends – including the increased use of capital (and technology) to foster production of goods and services, the outsourcing of higher-paying manufacturing jobs to lower-wage markets, and decreases in the top income tax rates – have all been factors that have led to higher wealth inequality in the United States.

There are solutions, but they may be hard for our society to embrace. For example, substantially increasing the minimum wage (and tying it to inflation, for future years) has long been sought by many. Personally, I believe that the inability of wages to keep pace has largely been a consequence of the dramatic increases in health care costs borne by corporations. (We need to address the structure of our health care system in a major way, as it is highly inefficient and consumes far greater of our GDP than seen in other developed countries of the world.) Still, if wages stay low, consumer spending (which accounts for 70% of all U.S. economic activity) will also continue to trend lower. In essence, you can’t expect to be able to sell goods and services if an ever-increasing share of the population can’t afford to purchase them.

My greater worry is that, as a society, we are not anchored by a common set of understandings and facts. In large part this is due to the rise of alternative media sources, including but not limited to social media, and the rise of monied interests seeking to influence public opinion (and, thereby, public policy). This has resulted in a level of incensed political discourse we have not seen for many decades.

I fear the consequences of this increased ability by business interests and the ultra-wealthy to influence the minds of so many Americans, often through disinformation campaigns, but also by not just presenting both sides of an issue, or by ignoring certain news events that deserved greater attention. I also fear the long-term consequences of the U.S. Supreme Court’s Citizens United decision, which unleashed a flood of contributions to political campaigns by corporations and the ultra-rich. As a frequent visitor to the halls of Congress in connection with my public advocacy efforts on behalf of individual investors, I can personally attest that monied interests possess great influence in the crafting of public policy and legislation, as well as substantial influence as to the rules adopted by U.S. government agencies.

Don’t get me wrong. I favor capitalism. Yet, unconstrained, capitalism leads to abuses. As James Madison long ago observed, “If all men were angels, no government would be necessary.” Prudent regulation, with a light touch, can be proper. Still, I believe government cannot be the solution to every problem, and government should be constrained in its size and should be as efficient as we can make it. A proper balance must be sought.

Cameron Murray, in his review of Peter Turchin’s 2015 book, Ultrasociety: How 10,000 Years of War Made Humans the Greatest Cooperators on Earth, observed that when “selfish elites and other special interest groups capture the political agenda … [t]he spirit that ‘we are all in the same boat’ disappears and is replaced by a ‘winner take all’ mentality. As the elites enrich themselves, the rest of the population is increasingly impoverished. Rampant inequality of wealth further corrodes cooperation.”

It is this decline in cooperation among Americans – our sense of a common social identity, and that some actions should be taken to foster not our own individual economic agendas but for the good of all of us – that I fear.

I worry that our current U.S. Constitution, while a great document, may not be up to the task of countering these trends. Changes to the U.S. Constitution I would like to see include: (1) term limits for all members of the U.S. Congress (for a maximum of twelve years), to better ensure statesmanship rather than blind allegiance to party doctrine; (2) limits on political contributions to any political campaign or cause to a set dollar amount, per person, per year, and the elimination of political contributions by corporations, unions, and other organizations; and (3) the adoption of multi-member districts for elections, which should give rise to more than two major political parties in the United States.

There are other solutions to the current political discord in our society, and to the threat of social upheaval that could result from the current levels of wealth inequality and its prospects for further severity. I hope that, in the years ahead, we (regardless of political allegiance or preferences) can find ways to have intelligent conversations about these issues, and that we can both identify and implement proper solutions.

While there are many long-term economic concerns, both within the U.S. and globally, I am struck by the rise of solutions, that in turn should benefit Americans by lowering costs, increasing productivity, and (hopefully) increasing standards of living:

· Self-driving cars, while still years (if not a decade or more) from widespread deployment, will lead to greater mobility for many persons in our society. It will also obviate, for many, the need to own a car or other vehicle (the annual average costs of ownership being about $9,000 a year, on average), and lead to transportation costs declines for many individual Americans.

· Low mortgage rates in recent years – and especially this year – has resulted in many residential mortgages being refinanced. For at least the next ten years, if not longer, this will decrease the housing costs of many Americans. In turn this will free up families to spend money in other ways. Lower interest rates on some other forms of consumer debt (car loans, student loans) will also help, to a lesser degree.

· With the rise of (somewhat controversial) fracking to mine oil and natural gas, America’s dependency on oil imports has declined significantly, and largely served to limit increases in the cost of oil (despite repeated attempts by OPEC to reduce supplies). And the increase deployment of hybrid vehicles and other more efficient vehicles has led to a modest decline in the demand for oil. Electric cars will likely be able to be purchased for a similar price as gas-powered cars by 2025, and further developments in battery technology will lead to ever-increasing ranges and shorter re-charging times over the next decade.

o Note that in much of western Europe the sale of gasoline-powered cars will be banned after 2030 or 2035. In September of 2020, California governor Gavin Newsom announced he was banning the sale of internal-combustion-engine passenger vehicles after 2035. It is likely that further bans on gasoline-powered vehicles will be enacted here in the United States, as well as other countries, especially after the costs of electric vehicles decline, and a much greater re-charging network is put in place (including at apartment complexes, condominiums, as well as for longer road trips).

· The continued decline of wholesale solar energy costs will cap the long-term costs of electricity in the United States, and greater deployment for individual home solar panels, will occur over the next two decades. Declines in the costs of other renewable energy resources (wind power, geothermal) and long-term energy storage (pumped hydro, flow batteries, and many more) will continue to shift our reliance away from fossil fuels and to these “renewables.” The shift will primarily occur due to basic economic considerations, although continued tax incentives for renewable energy will likely hasten the shift somewhat.

· With the rise and deployment of computers from the 1980’s forward, productivity enhancements have taken place. We continue down this “computer revolution” through ever-more-sophisticated computer software applications. Manufacturing in the United States will benefit, as greater robotics, more stable supply chains, and less lesser finished product transportation costs combine to make manufacturing in the United States less expensive.

o But, due in large part to the continued deployment of robotics, the number of manufacturing jobs may not increase substantially. Instead, we will need even more engineers and computer programmers.

· Advancements in medicine, especially the application of genomics and technologies to drive vaccines will continue to lead to cures and therapies for many chronic illnesses. Life expectancies will continue to increase. The majority of students graduating from college this coming year will likely live to at least age 100.

If I had to sum up the prior two sections, I would conclude:

First, the U.S. economic recovery from COVID-19 will take time; it will start off strong by March or April of 2021, and the statistics thereafter will appear good. But it will take time to reach the very low unemployment levels seen prior to the start of the pandemic. A shock to both the ability to supply goods and services, as well as the ability of consumers to purchase such goods and services, has occurred. Overcoming these shocks will take time, and government support for spending (such as through infrastructure improvements) to counter the demand shock (especially) is far from certain.

Second, over the long term many positive economic trends have emerged that will promote U.S. economic growth and may lead to longer lives and greater living standards. How the U.S. addresses its accumulated governmental debt remains a risk, however, especially if interest rates increase and a “debt spiral” emerges.

So, how does all of this affect your investment portfolio?

I often get asked (rarely by my clients, but often by others) as to what the stock market will do in the nearfuture – such as during the next week, month, or year? The answer … I have no clue. And I don’t think anyone else has a working crystal ball, either – at least a consistently working one.

Yet, I do believe that current valuation levels in the capital markets lead to a likely range of possible long-term returns among different asset classes. And that we should take such projections into account when making financial decisions – such as projecting the long-term sustainable rate of withdrawal from the portfolio of a person who has recently retired.

U.S. small cap value stocks, foreign developed markets stocks, and emerging markets value stocks possess long-term (10-year or 15-year) projected average annualized returns that are quite favorable – and in the range of 8% to 10% (on average). There will be a lot of “ups” and “downs” along the way, however.

In contrast, both U.S. and foreign large cap stocks (overall, in a “balanced” or “core” composition), and in particular U.S. large cap growth stocks, are extremely overvalued at present.

A portfolio which “tilts” toward small cap, value stocks, and which incorporates emerging markets value stocks, possesses a high probability (perhaps 80% or greater) of outperforming the overall U.S. and foreign stock markets over the next 10-15 years.

While the academic evidence does not support the ability of market forecasters to consistently predict short-term returns of asset classes, or of specific securities, we can somewhat predict the likely returns of various stock asset classes over the next 10 or 15 years. The further in time out we go, the more likely “reversion to the mean” of asset class valuations will occur, and the range of projected returns becomes narrower.

The resulting projections are just that – estimates. They are undertaken by combining the following analytical foundations:

· The historical returns of various asset classes, both over the very long-term (when such data is available) and over the past 20-30 years.

· An understanding of the drivers of equity returns, often called “factors,” with estimates of the future robustness of each factor in the future affected by the knowledge of each factor and the ability (or lack of ability) to engage in arbitrage with respect to such factor.

· Adjustments are made to estimated future returns based upon an assumed lower rate of inflation in future years, relative to that of the past several decades. However, should inflation be higher, then logically (to an extent) future expected returns of asset classes would also likely be higher, at least over the long term.

· It is assumed that U.S. economic growth will be at a lower rate in the future, given the decline of the rate of U.S. population growth in recent years and as projected into the future. Also, the substantial drag on future U.S. economic growth due to current high levels of federal and state government debt, corporate debt, and personal debt is considered.

· An assumption is made that “reversion to the mean” will occur with regard to current asset class valuations by the end of the 10-year or 15-year period for which estimates are provided. In itself, making such an adjustment is somewhat difficult, as the means of asset class valuations change over the very long term. In addition, rarely does an asset class valuation exist at the mean. Undervaluations of asset classes can and do occur, often 50% or more below the mean, and often 100% or greater above the mean. In itself, this implies that the possible range of average annualized returns for any one asset class is quite broad, and the resulting returns for any particular asset class could be much higher or much lower than the estimates provided, even over any 10-year or even 15-year period of time.

In other words, to put it simply, the projections provided of asset class returns are merely estimates, and the actual asset class returns that will occur will often be far different from what is estimated.

Even with all of those limitations, I believe that projections of asset class returns are useful. They force us to consider, at least for financial planning purposes, a somewhat more accurate set of long-term asset class projected returns than that we might otherwise erroneously assume from just assuming past (historical) long-term returns will continue into the future. When, as currently exists, many asset class valuations appear to be much higher than normal, this instills into our financial planning processes a more conservative analysis in determining whether lifelong financial goals can be obtained.

For many years I have used my own methodology to project 15-year probable returns for U.S. stocks – large cap vs. small cap, and growth vs. balanced vs. value. My own methodology relies on price-book valuations, relative to historic levels over the past 43 years. In the chart below, I provide my projections of future U.S. stock asset class returns, as of December 10, 2020.

For comparison purposes, Research Affiliates, a firm that does extensive modeling on future returns of different asset classes, projects the following average annualized returns over the next 10 years. In the chart on the next page, I provide a summary of my own and excerpts from their data.

(Be aware that the asset class formation metrics used by Research Affiliates are somewhat different that that utilized in my own data set, as well as their methodology for determining historical and present valuation levels and adjustments that lead to expected returns projections.)

ASSET CLASS | Ron’s 15-Year Projected Average Annualized Returns (as of Dec. 10, 2020) | Research Affiliates’ Estimated 10-Year Average Annualized Returns (as of Nov. 30, 2020) | Research Affiliates’ Estimated 5-Year Average Annualized Returns (as of Oct. 1, 2020) |

U.S. Large Cap Growth Stocks | -5.1% | | |

U.S. Large Cap Balanced Stocks | 3.9% | 2.0%* | |

U.S. Large Cap Value Stocks | 5.8% | | 8.2%** |

U.S. Small Cap Growth Stocks | 1.1% | | |

U.S. Small Cap Balanced Stocks | 9.3% | 5.1%* | |

U.S. Small Cap Value Stocks | 10.2% | | 10.3%** |

Foreign Developed Markets Stocks (EAFE Index) | | 8.5%* | |

Foreign Emerging Markets Stocks (MSCI EM Index) | | 6.7%* | |

U.S. Treasury Long-Term Bonds | | -1.5% | |

U.S. Treasury Intermediate Bonds | | 1.6% | |

U.S. Short-Term Bonds | | 1.4% | |

Real Estate Investment Trusts (REITs) | | 4.0% | |

Research Affiliates’ data is excerpted from their analysis atResearch Affiliates, LLC (“Research Affiliates”) © Research Affiliates 2020.

PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RETURNS.

THE EXPECTED RETURNS SHOWN ABOVE ARE ESTIMATES ONLY; THE ACTUAL RETURNS CAN BE, AND IN MANY INSTANCES WILL BE, QUITE DIFFERENT FROM THE ESTIMATES PROVIDED ABOVE.

* Given the December month-to-date returns of stocks, ranging from 0% to 5% depending upon asset class, as of Dec. 10, 2020, the projected 10-year returns for stocks would likely be a bit lower as of Dec. 10, 2020.

** Given the fourth quarter-to-date returns of U.S. Large Cap Value stocks (17% to 18%, using DFA U.S. Large Cap Value Portfolio as a proxy) as of Dec. 12, 2020, the projected 5-year returns should be substantially less as of Dec. 12, 2020. Given the quarter-to-date returns of U.S. Small Cap Value stocks (29% to 30%, using DFA U.S. Small Cap Value Portfolio as a proxy), the projected 5-year returns should be substantially less as of Dec. 10, 2020.

Nominal, not real (inflation-adjusted) returns are set forth. All data presented sets forth expected (estimated) gross returns, and does not reflect trading costs, mutual fund fees, nor any investment advisory fees charged by Scholar Financial.

For educational purposes only. Before relying on any of this data, seek the advice of a qualified investment adviser to more fully understand the purposes of this data, its proper utiization, and its inherent limitations.

A widely followed indicator of the valuation level of U.S. large company stocks is the Shiller PE10 Ratio, which (as of Dec. 29, 2020, 4pm ET) stands at 33.93 – 100% higher than its historical mean (from 1870 to present) of 16.76.

This implies a negative return for U.S. large company stocks over the next eight years, assuming reversion to the mean.

While there are some reasons to speculate that a more accurate historical mean of the Shiller PE10 ratio may be around 22 (due to changes in accounting methods over time), we still end up with a very high overvaluation of U.S. large company stocks – at least 50% above the long-term mean.

The last time I observed such a disconnect between “growth stocks” and “value stocks” was in early 2000. History has a way of repeating itself. And, this time, the disconnect appears to be even worse.

As indicated previously, over the next 15 years I anticipate U.S. large cap value stocks will deliver modest returns (about 5-6% annually, on average), while U.S. small cap value stocks will deliver stronger returns (about 10% annually or greater, on average). However, these are estimates only, and the actual returns seen over the next 15 years will likely be quite different from these projections.

6) Emerging Markets Value Stocks.

By many estimates U.S. stocks are overvalued, relative to stock markets in other countries.

Yet, the same bubble in certain stocks in the U.S. has been repeated abroad. Stocks of large “growth” companies in emerging markets have often seen valuation levels that can only be viewed as “excessive” – similar to stocks like Tesla.

Still, as of early December 2020, investors were paying roughly twice as much per dollar of earnings for U.S. equities as they are for stocks in emerging markets, as computed by CAPE ratios.

As Jeremy Grantham of GMO notes, “internationally – both in developed and emerging markets – Value also looks like a remarkable bargain … In many cases, in fact, we have never seen cheap stocks looking cheaper than they do today.”

It is not surprising that the highest expected returns over the next 10-15 years may exist in “emerging markets value” stocks. The demographics of emerging markets countries appear quite favorable relative to western Europe and the United States, with greater increases in populations in most countries, along with a continued migration away from a commodity-export and agricultural economy to a modern economy. In additions, excluding some of the very large “growth” stocks found in those markets, on a relative valuation basis emerging markets stocks appear quite “cheap.”

Perhaps the largest challenge to individual investors has been the long decline in interest rates, and the relatively low rates over the past twelve years. Vastly different opinions exist as to whether low interest rates will persist in the United States for many years to come, or whether interest rates will increase, or even decline here in the United States to negative interest rates (for U.S. Treasuries).

Quite frankly, it is nearly impossible to predict the future of yields on fixed income investments. And, despite many warnings over the past decade of a surge in inflation, such has not occurred, and the future of inflation (a measure of the rise in prices of consumer goods) is also very difficult to predict.

I can observe that yields for bank’s certificates of deposit have fallen over the past year, as well as yields on short-term and mid-term municipal bonds. Current yields for short-term debt instruments in the U.S. are near their historic lows – over the past 60 years!

I continue to urge investors to be wary of long-term bonds. If and when yields on bonds rise, the value of bonds (especially long-term bonds) will fall.

Additionally, seeking out higher yields by purchasing lower-quality bonds, whether issued by municipalities or by corporations, does not seem worthwhile at present. Simply put, the small amount of additional return provided does not appear to justify the additional risks of default that are undertaken. Risk among lower-rated fixed income securities appears to be misplaced at present.

As I have written about previously, the SWAN ETF, which is designed to possess about 90% U.S. Treasury securities (safe, intermediate-term bonds) and about 10% call options on the S&P 500 Index, appears to be one place higher returns can be obtained. I concluded my initial research on the SWAN ETF about 18 months ago, and continue to review new articles and academic research on the strategy used by the fund. The SWAN ETF is a good holding to replace a portion of the fixed income component of an investor’s portfolio.

For example, an investor who is retired and possesses a 50% allocation to stocks (via stock mutual funds and stock ETFs) might allocate 25% of the portfolio to the SWAN ETF, while keeping 25% in short-term, high quality bond funds and/or certificates of deposit and/or municipal bonds.

· In essence, the short-term and safer fixed income investments are the top layer of a three-layer cake portfolio, and it is from this top layer that withdrawals are undertaken.

· The SWAN ETF could be thought of as the middle layer of the cake, for while this fund has some short-term volatility, over any given 5-year period there is only a small probability of negative returns (and, even then, the negative returns would not be severe). Transfers would occur from the SWAN ETF to the top layer as “rebalancing” the portfolio is undertaken periodically.

· The bottom layer, designed for utilization in 10 years or greater, is allocated to stocks (via highly diversified stock mutual funds and ETFs). Transfers from the bottom layer to the SWAN ETF (middle layer) would also occur through the rebalancing process, such as when equities (stock mutual funds) had a period of very good returns.

A younger investor, willing to assume more risk, and with 20 or greater years to go until retirement, might invest 80% of their portfolio in equities, and 20% in the SWAN ETF.

An investor with a much higher rate of withdrawal from their investment portfolio, such as 5% to 7% a year, might prefer a much higher allocation to the SWAN ETF, while decreasing their equity exposure down to the 20% to 35% range.

(Of course, each investor’s situation is unique. Some investors possess higher degrees of tolerance for risk; other investors possess higher or lower need to take on risk. Considerations such as employment stability, diversification of income streams, and many more are taken into account prior to suggesting a particular strategic asset allocation for any investor.)

As my clients are aware, I have favored the use of equity (stock) mutual funds from Dimensional Funds Advisors for years, in large part due to their greater exposures to certain “factors,” their close control of trading costs, and their conservative approach to securities lending while keeping all net securities lending revenue in the fund (rather than sharing a portion thereof with the investment adviser to the fund, which results in a "hidden" cost to fund shareholders).

In just the recent few years, more "multi-factor" funds, as well as multi-factor separate account strategies, have launched and become available to a greater number of investors. There are, however, often dramatic distinctions in how the factors are combined by the investment manager. In fact, in my own view, much more academic research is required on how to best utilize multiple factors.

Even lacking the volume of academic evidence I would like to see - on the best way to combine (and utilize) factors - the emergence of so many multi-factor funds and ETFs and other vehicles brings forth new competition in the marketplace, which has a tendency to result in lower fees and costs for investors.

In some very positive developments for our clients, recently Dimensional Funds Advisors (DFA) reduced the fees of several of its mutual funds.

And also – for several of DFA's mutual funds which will be converted to ETFs – reduced the “tax drag” on investor returns for 2021 and forward by migration to a new fund structure.

To achieve greater tax efficiencies, some of DFA's tax-managed and/or tax-aware mutual funds are being transitioned to the “exchange-traded fund” (“ETF”) structure. (The reason for this involves how “accumulation units” are “redeemed” in the ETF structure, resulting in the ability to transfer low-cost-basis stocks out of the ETF to a tax-exempt investor, thereby benefiting other shareholders within the ETF. A full explanation of how this works involves many pages, which I will skip in an attempt to keep this section brief. Suffice to say that this is a "tax loophole" that benefits the ETF structure, compared to most mutual fund structures.)

Dimensional’s stock mutual funds have historically had low long-term capital gains distributions given its broadly-diversified, low turnover approach. And DFA’s tax-managed and tax-aware funds have done a very good job of securing “qualified dividend” treatment where possible, which effectively lowers the tax rates applied to distributed dividends. The switch to ETFs will enhance the ability of these funds to limit long-term capital gain distributions, with distributions of capital gains each year likely to fall to zero or close to zero. In effect, this reduces the “tax drag” on the investment returns of these funds/ETFs, when held in taxable accounts.

Here is a chart that details recent and upcoming changes to some of Dimensional’s funds:

Former Fund | Replacement ETF | Old Annual Expense Ratio | New Annual Expense Ratio |

Tax-Managed U.S. Equity Portfolio | Dimensional U.S. Equity ETF | 0.18% | 0.08% |

Tax-Managed U.S. Small Cap Portfolio | Dimensional U.S. Small Cap ETF | 0.40% | 0.30% |

Tax-Managed U.S. Targeted Value Portfolio | Dimensional U.S. Targeted Value ETF | 0.40% | 0.30% |

Tax-Aware U.S. Core Equity 2 Portfolio | Dimensional U.S. Core Equity 2 ETF | 0.20% | 0.16% |

Tax-Managed International Value Portfolio | Dimensional International Value ETF | 0.45% | 0.30% |

Tax-Aware World ex-US Core Equity Portfolio | Dimensional World ex-U.S. Core Equity 2 Portfolio | 0.30% | 0.25% |

You are not required to undertake any action to have your mutual funds converted to the lower-cost, more tax-efficient ETFs. This will be done automatically for you, and at no cost to you – nor any tax consequence arising from the conversion.

In addition, Dimensional has launched three new ETFs with somewhat lesser factor exposures and with relatively low annual expense ratios.

Dimensional US Core Equity Market ETF (DFAU) | 0.12% | Listed: 11/18/20 |

Dimensional International Core Equity Market ETF (DFAI) | 0.18% | Listed: 11/18/20 |

Dimensional Emerging Core Equity Market ETF (DFAE) | 0.35% | Listed 12/2/20 |

As always, obtain the read each fund's Statutory Prospectus, Statement of Additional Information, and Annual/Semi-Annual Reports, to fully understand any mutual fund or ETF prior to investing in same. Important is achieving an understanding the investment strategy of the fund itself, but also how a fund is properly utilized in the design of an overall portfolio. Again, this information is presented for educational purposes only; prior to the application of this information to your own investment portfolio, seek the advice of a qualified investment adviser.

As always, thank you for the opportunity to share these thoughts.

Ron

Ron A. Rhoades, JD, CFP®

Personal Financial Advisor

Scholar Financial